Market Chat: Panamax Newbuilding Orders Reach Record Highs

Surge in Panamax newbuilding orders

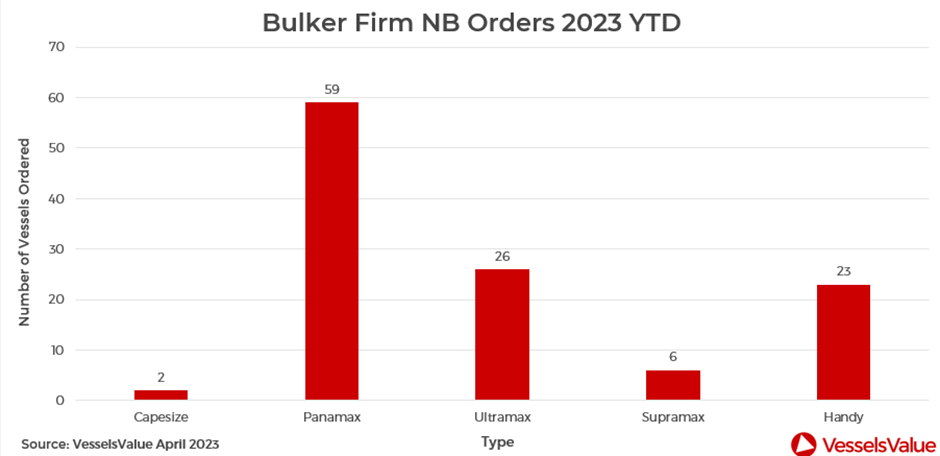

There has been a surge in Panamax newbuilding orders in the first four months of 2023. So far this year there have been 61 orders placed, compared to just 13 for the same period in 2022, an increase of c.369%. The majority of these orders have been placed since March, coinciding with an uptick in Bulker spot earnings as confidence in this sector begins to grow once again. After falling to a two and a half year low of around 5,900 USD/Day in February, spot rates have more than doubled to reach around 13,600 USD/Day, an increase of c.131%.

The overwhelming majority of these orders have been placed by Chinese companies, accounting for c.71% of orders. Canada ranks second with c.13% of orders and Greece ranks third with c.7%. Denmark, Japan and unknown buyers account for the remainder with a share of c.3% each. More than three quarters of these orders are being built in China, with a share of c.87% with the remaining 13% scheduled to be built at Japanese yards.

Continuing on the upward trend, newbuilding values for vessels of 82,000 DWT are up c.6.7% from the start of the year from USD 31.10 mil to USD 36.38 mil. Demand for Bulkers has picked up following the reopening of China from Covid-19 restrictions. There is plenty of optimism that there will be a rebound in the domestic economy which should provide a boost to commodity demand, and this has been supporting rates in recent weeks. The push towards Green technology and more efficient vessels in order to comply with the new CII regulations from the IMO is also behind many newbuilding orders, including the recent 12 x Panamax BC of 82,000 DWT ordered by Shandong Shipping at Jiangsu New Hantong Ship Heavy Industry and scheduled to be delivered in 2025, sold en bloc for USD 33 mil each, VV value USD 31.16 mil. These vessels will be equipped with carbon capture and storage technology developed by the China State Shipbuilding Corporation, in a push towards reducing carbon emissions within the Shipping industry.

There has also been increased demand for Panamax wood pulp carrier newbuildings which are achieving premiums due to their specific design, notably 10 x Panamax BC of 84,500 DWT ordered by CITIC Financial Leasing at Chengxi Shipyard, sold en bloc for USD 50.15 mil each, VV value USD 38.49 mil.

Values for 20YO VLCCs continue to firm

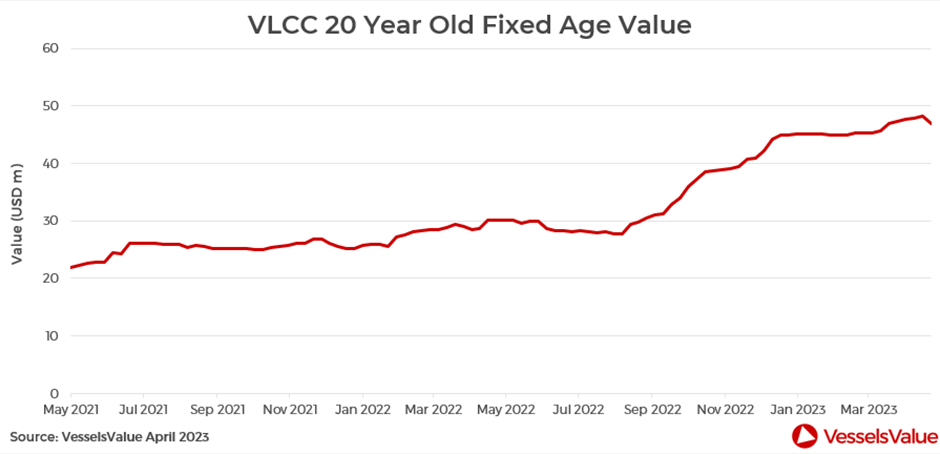

Values for VLCCs have risen across all age categories since the start of the year. Due to a continued firming in spot rates, this time last year the TD3c-TCE – Middle East Gulf to China route was at -1,307 USD/Day and at time of writing this has rebounded to 41,807 USD/Day.

Values for 20YO VLCCs are up by c.4.5% from the start of the year and up by c.56% YoY from a demolition value of USD 30.18 mil USD to USD 47.15 mil. Fixed age values for this age range have risen steadily since July 2022 and are now levels not seen since August 2008.

So far this year, there have been 30 secondhand VLCC sales reported and the average age for vessels sold is 17 years, as the demand for older, more cost effective tonnage continues, in order to trade Russian crude cargoes that have been sanctioned by the EU and G7.

Notable sales include the Princess Mary (306,200 DWT, June 2004, Mitsubishi HI) that sold to unknown Chinese buyers for USD 51 mil, VV value USD 50.92 mil. Hellenic Tankers bought this vessel in 2018 for less than half the price that it was sold for this month at USD 22.7 mil. This demonstrates the extremely strong demand for this sector as sentiment from recent sales continues to set the benchmark higher.

VesselsValue data as of April 2023.

Disclaimer: The purpose of this blog is to provide general information and not to provide advice or guidance in relation to particular circumstances. Readers should not make decisions in reliance on any statement or opinion contained in this blog.

Want to know more about how our

data can help you assess the market?