Market Chat: Week 6

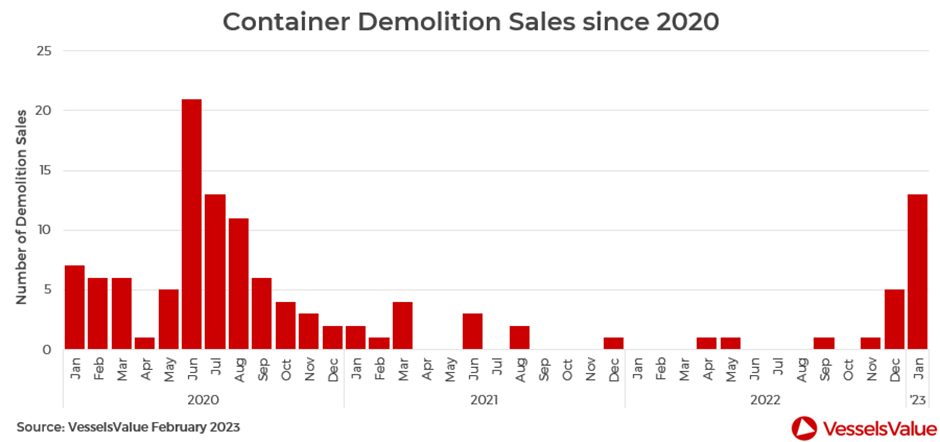

Container demolition

January was the busiest month for Container demolition sales since July 2020. All sales reported were on the smaller scale, with four Feedermax vessels committed and nine Handy Containerships setting sail for their final voyage to be recycled in India.

All Container vessels scrapped were built in the 1990s with an average age of 1996, indicating that owners are only scrapping what is absolutely necessary. After reaching an 18 month low in December, scrap prices firmed once again in January, with an average of 580 USD/LDT. With values for Feedermax vessels down c.64% year on year to a January average of 11,579 USD/Day, this provides incentives for owners looking to scrap their oldest and least efficient vessels.

Notable sales include the SSL Kochi (1,725 TEU, June 1998, Daewoo) that sold for 580 USD/LDT, VV Demo value 580 USD/LDT also the Sol Delta (1,728 TEU, June 1995, Stocznia Szczecin Nowa) that sold for 587 USD/LDT, VV Demo value 570 USD/LDT.

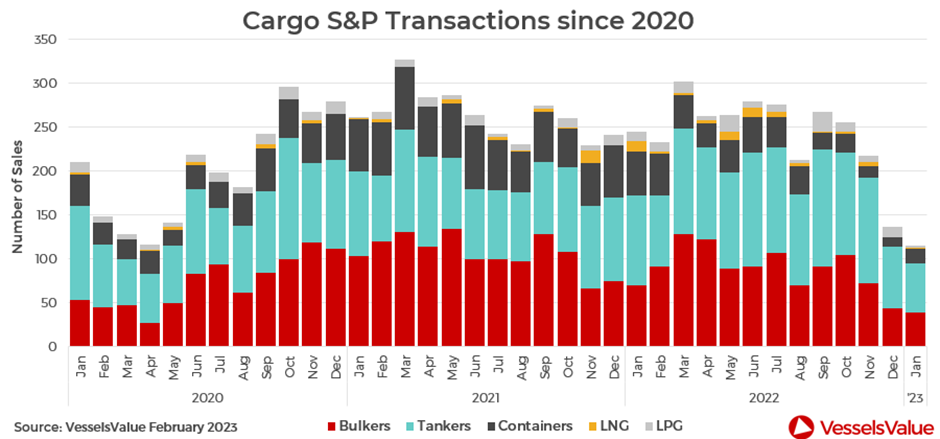

S&P transactions fall to two and a half year lows

Cargo sale and purchase transactions have been at the lowest levels since Q2 2020 in December and January. Traditionally, December and January represent a seasonal downturn for the sale and purchase market due to various holidays across the globe. However, transaction levels have been steadily declining since the peak in July, where 265 sales were reported. Almost half of the sales were in the Bulker sector, 31% in the Tanker sector, 13% in Containers and the remaining 7% in the Gas sector.

In January, sales were split evenly between Bulkers and Tankers, accounting for 41% each, followed by Containers at 15% and Gas at 3%. Overall, there were 116 sales reported, a slight increase from December with a two and a half year low at 114 sales.

There is still plenty of demand for Tankers, but with values still at very high levels, the focus is on older, more cost effective tonnage. In contrast, the Bulker sector is eagerly waiting to see what happens in China in respect to the relaxing of Covid-19 regulations, if and when there will be further stimulus measures to kickstart the economy. On the Container side, the market has yet to bottom out, and the charterers are no longer there to provide longer term fixtures at the rates that we saw last year.

VesselsValue data as of 10th February 2023.

Disclaimer: The purpose of this blog is to provide general information and not to provide advice or guidance in relation to particular circumstances. Readers should not make decisions in reliance on any statement or opinion contained in this blog.

Want to know more about how our

data can help you assess the market?