Newbuild Report 2021

Introduction

2021 was a record breaking year for the Maritime industry. The spread of three major Covid-19 variants had substantial repercussions for Shipping: labour shortages, port congestion and volatile oil demand, to name but a few.

Responding to the fast changing nature of global trade, the newbuilding orders of 2021 have reflected a world littered with restrictions on movement, geopolitical uncertainty and an increasingly prominent Green agenda. Whilst lockdown consumerism has led to unprecedented Container demand, crude products have taken a backseat. An ongoing energy crisis is driving the addition of essential Gas carriers to the orderbook, the full impact of which will only materialise in the coming years.

Cargo

The Cargo vessels covered in this report are Containers, Bulkers, Small Dry, Tankers and Gas.

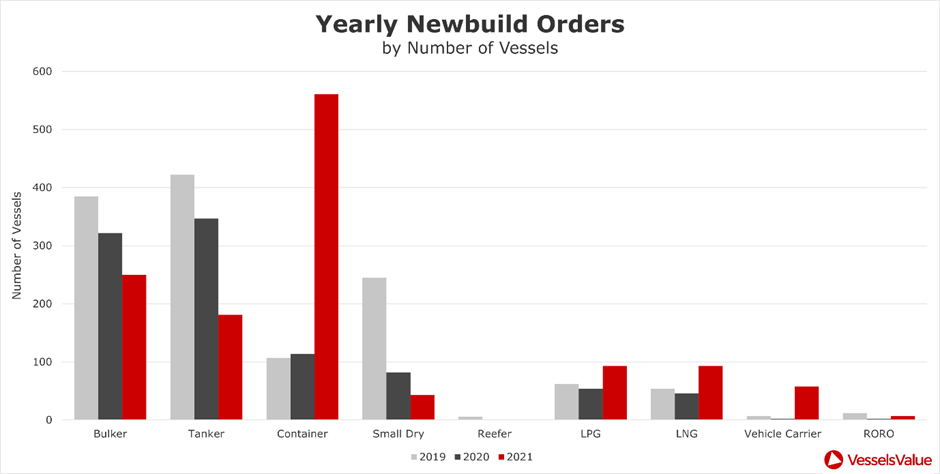

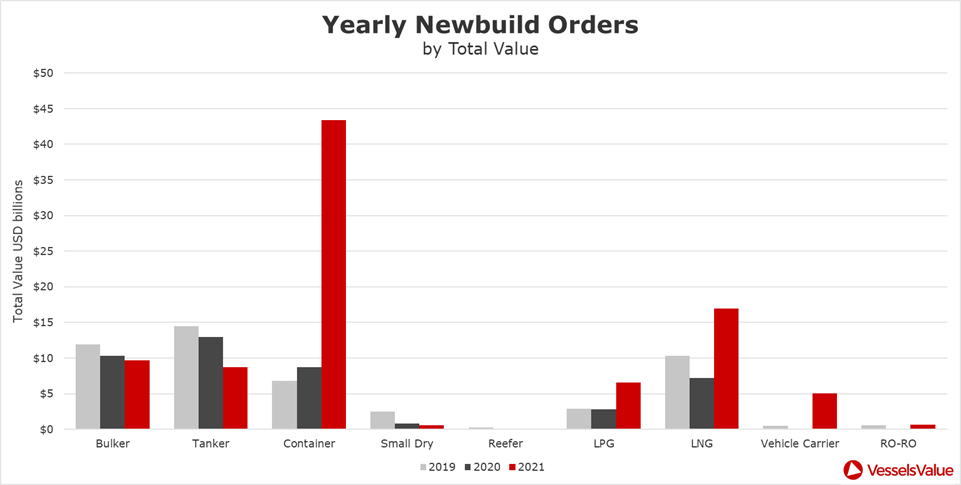

1,286 vessels were added to the orderbook in 2021, a 32.7% increase from the 969 vessels ordered in 2020. This is paired with an extraordinary growth in price for certain vessels. 2020’s total orderbook was worth USD 42.83 bil, compared to 2021’s USD 91.61 bil, a staggering 114% increase.

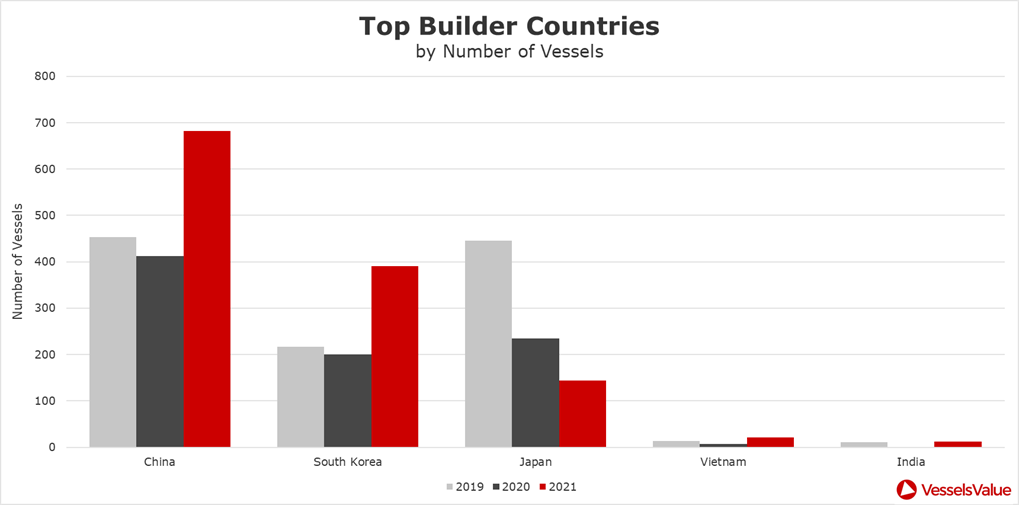

As expected, the large majority of vessels ordered in 2021 are to be constructed at yards in China, South Korea and Japan. The number of vessels confirmed in these three countries totals 1,217; 682 in China, 391 in South Korea and 144 in Japan. Other notable builder countries are Vietnam and India, with 21 and 12 vessels respectively.

Containers

The biggest story of 2021 was the vast number of Container vessels ordered. By the end of 2020, governments worldwide began to open their economies following the first wave of Covid-19. With this came the release of extraordinary pent up consumer demand for products shipped in Containers.

A primary implication of this increase in demand was port congestion on both sides of the Pacific. Poor weather and Covid-19 restrictions at Asian terminals exacerbated the effects of hefty queues into Los Angeles and Long Beach, California. This shortened vessel availability, contributing to record high freight rates and vessel earnings. Consequently, values for Containers rocketed. After years of dwindling earnings for these assets, owner investment in newbuilding was seen as a sensible use of increased revenue.

561 Container vessels were ordered in 2021 compared to 114 in 2020 and 107 in 2019 (see Figure 2). 2021’s boxship orders amounted to USD 43.39 bil, 47.4% of the year’s total and surpassing the entire Cargo fleet orderbook value of 2020. Asia accounted for the majority of 2021 Containership orders, with Taiwan, China, Singapore, South Korea, and Japan ordering 314 vessels between them, 65.8% of the global total.

The biggest spenders on Containers came from Taiwan. 2021 saw 131 orders for a total of USD 8.38 bil. Their 2019 and 2020 additions to the Container orderbook only totalled 58 vessels.

As owners competed for their slice of the earnings boom, builder capacity tightened with the explosion in Container orders, inflating newbuild prices. In September 2020, a 4,250 TEU Panamax Container order cost USD 23.6 mil. By September 2021, this same order cost USD 65.5 mil, a staggering 177.7% increase.

Headline Orders

25th March 2021, 20 New Panamax Containers (15,000 TEU, 2024/2025, Samsung) ordered by Evergreen Marine for USD 2.48 bil.

20th April 2021, 4 ULCVs (24,100 TEU, 2023, Jiangnan Shanghai Changxing HI) ordered by MSC for USD 600 mil.

28th June 2021, 12 Panamax Containers (3,055 TEU, 2023, Nihon Shipyard) ordered by Wan Hai Lines for USD 585.6 mil.

22nd September 2021, 10 Post Panamax Containers (7,000 TEU, 2024, Shanghai Waigaoqiao Shipbuilding) ordered by Seaspan Corporation for USD 860 mil.

Bulkers

The Bulker market had a successful end in 2021, with the 54-TCA (Capesize spot earnings) hitting 86,953 USD/Day in October, heights not seen since 2009. However, this late surge, partially caused by the Asian port congestion and increased coal trade, did not translate into newbuild activity like that seen in the Container sector.

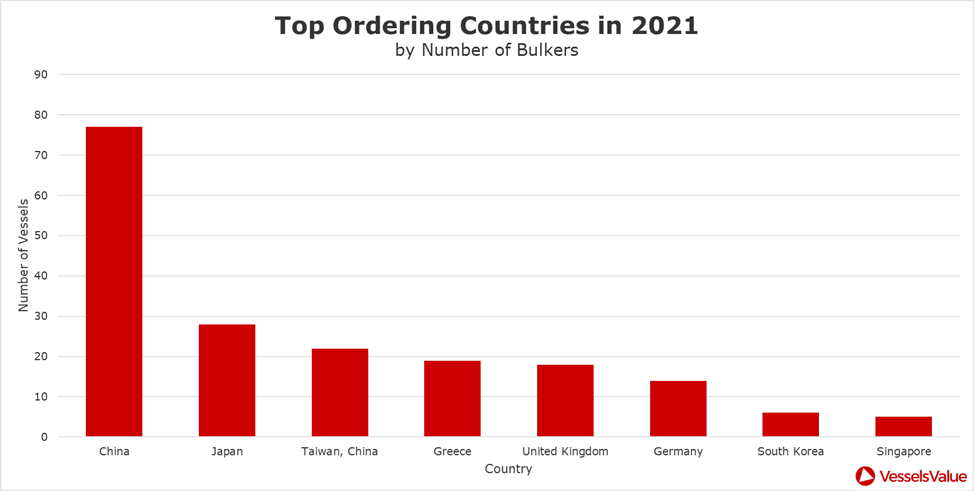

In fact, the number of Bulker newbuild orders placed dropped from 322 in 2020 to 250, resulting in a total 2021 Bulker orderbook worth USD 9.7 bil. Chinese buyers accounted for 77 of these Bulker orders, 30.8% of the total, followed distantly by Japanese buyers with 28 orders (see Figure 3). This is in stark contrast to 2019 where the Japanese surpassed Chinese orders by 18 vessels, representing a significant reduction of Japanese investment in the Bulker newbuild market.

Compared to previous years’ Bulker newbuild activity, there has been a distinct drop in demand for new vessels in 2021. The revitalised Container market diverted interest away from larger Bulk carriers, slowing the addition of tonnage to the live fleet. This cap on supply could bode well for higher freight rates in the near future.

Headline Orders

16th April 2021, 10 Panamax Bulkers (82,000 DWT, 2022/2023, Jiangsu Hantong Ship Heavy Industry) ordered by Nisshin Shipping for USD 280 mil.

14th June 2021, 12 Capesize Bulkers (209,800 DWT, 2023/2024, New Times Shipbuilding) ordered by Himalaya Shipping for USD 804 mil.

14th October 2021, 8 Ultramax Bulkers (63,600 DWT, 2023, COSCO Shipping Heavy Industry Shanghai) ordered by Bank of Communications Financial Leasing for USD 256 mil.

Small Dry

The Small Dry sector was negatively affected by Covid-19, with huge numbers of orders postponed or cancelled. This resulted in a sharp drop off compared to previous years. 2021 made up 43 of the 370 total vessels ordered over the last 3 years, just 11.6%. Pandemic stricken 2020 and 2021 saw 125 Small Dry vessels ordered for a combined USD 1.38 bil, compared to 245 ordered vessels in 2019 alone, worth USD 2.49 bil.

Headline Order

21st September 2021, 6 General Cargo vessels (5,400 DWT, 2023/2024, Chowgule) ordered by Atobatc for USD 81.6 mil.

Tankers

If the Container sector was 2021’s winner, then the Tanker sector was its loser. The global response to Covid-19 drove crude product demand into the ground, creating an oversupply of tonnage that kept vessel earnings at low levels. The TD3C-TCE (VLCC spot earnings) tumbled to -6,779 USD/Day in March 2021 as China’s oil demand dropped annually for the first time in two decades. Owners and operators struggled to break even for much of the year.

The response to this earnings slump was a huge drop off in newbuild orders. 2021 saw 181 Tanker orders worth USD 8.68 bil. This placed the Tanker sector behind Containers, LNG and Bulkers in terms of total 2021 orderbook value (see Figure 4).

As seen above, this is in stark contrast to previous years. 2019 saw 422 Tankers orders, representing a steep 57.1% drop over the three year period. With these 2019 ordered vessels set to launch in the near future, the dramatic shortening of newbuilding activity in 2021 is understandable as rates struggle to recover from the pandemic.

Despite the poor outlook, Greek investment in the Tanker sector has not substantially decreased. 2021 saw the Greeks order 49 vessels, 27.1% of the total, with only a small decrease from their 60 Tankers added to the orderbook in 2020. Of the 49 vessels, 18 were in the Aframax and LR2 sector. The number of Greek VLCC orders grew, with a purchase from Maran Tankers outlined below.

While Chinese buyers ordered 34.7% fewer Tankers than the Greeks, 32 compared to 49, the difference in value for the 2021 Tanker orderbook was down 64.3%; Greek orders totalled USD 2.77 bil and Chinese orders totalled USD 991 mil. This highlights a disparity in priorities: the Chinese focused on Small Tankers and MRs, whilst the Greeks kept up interest in larger crude and product carriers.

Headline Orders

4th February 2021, 4 VLCCs (300,000 DWT, 2023, Samsung) ordered by Maran Tankers for USD 417.2 mil.

29th April 2021, 4 Handy Chemical Tankers (33,000 DWT, 2023/2024, Dae Sun) ordered by ACE Tankers for USD 188 mil.

15th June 2021, 10 MR2 Tankers (50,000 DWT, 2022/2023/2024, New Times Shipbuilding) ordered by China Development Bank for USD 383.8 mil.

15th October 2021, 7 Aframax Shuttle Tankers (120,000 DWT, 2023-2027, Samsung) ordered by Rosnefteflot for USD 1.72 bil.

Gas

Gas carriers had a more than healthy 2021 in terms of newbuilding activity. 93 LPG and 93 LNG vessels were ordered, up from 54 and 46 respectively in 2020. The growth in demand for LPG vessels matches expected US production increases in the coming years, and the reversal in oil production cuts by OPEC is likely to be a key driver of Middle Eastern production.

LNG vessels saw a 207% increase in orders, totalling USD 16.98 bil, the most valuable addition to the Cargo orderbook in 2021 outside the Container sector. Soaring demand for LNG vessels is being fuelled by a global push towards green energy alternatives. With LNG having a smaller carbon footprint compared to traditional hydrocarbons, it is seen as a viable transition fuel.

Similarly, geopolitical uncertainty is influencing demand for gas carrying vessels. The ongoing energy crisis and the construction of Nord Stream 2 have raised concerns over Europe’s dependence on Russian gas. Future volumes imported from regions such as the US and the Middle East offer opportunity for reduced pipeline dependence, driving orders for LNG vessels.

Like the Tanker market, the Greeks are leading the way in terms of 2021 Gas sector investment. They take the lead for LNG orders, totalling 18 vessels worth USD 3.63 bil (see Table 1) and are only behind South Korea’s 16 LPG orders with 14. This is a vast increase in Gas expenditure for the Greeks, compared to the 1 LNG and 4 LPG vessels ordered in 2020.

Headline Orders

20th January 2021, 2 VLGC LPG (90,000 CBM, 2022/2023, Hyundai Heavy Ind.) ordered by undisclosed buyers for USD 151.8 mil.

15th April 2021, 3 Large LNG (174,000 CBM, 2024, Hyundai Heavy Ind.) ordered by Hyundai LNG Shipping Co. for USD 568.5 mil.

22nd October 2021, 4 Large LNG (174,000 CBM, 2024/2025, Samsung) ordered by Global Meridian Holdings for USD 826.1 mil.

7th December 2021, 3 Large LNG (174,000 CBM, 2024/2025, Hudong Zhonghua) ordered by United Liquefied Gas Shipping for USD 555 mil.

Offshore

The Offshore market remains heavily over supplied due to the high number of units built between the boom market of 2010 and 2014. There is little interest from owners, yards or financiers to place newbuild orders as many are still feeling the effects from the market downturn beginning in late 2014 and the more recent Covid-19 market.

Conclusion

In a record breaking year for the Maritime industry, the big winners are the Container and Gas sectors. 2021’s unprecedented box demand led to owners investing heavily, attempting to plug the supply gap. Similarly, environmental pressures and an ongoing energy crisis in Europe have encouraged investment in Gas carriers to sure up global energy supply chains, with a focus away from traditional, dirtier fuel sources like oil and coal.

This had a negative knock on effect for wet Cargo; Tankers have seen their rates at rock bottom, diverting newbuild activity away in what was a tough year for the sector. Dry Bulk orders were not as negatively impacted, with only marginal drop offs in ordering activity compared to 2020. The Offshore sector, meanwhile, is continuing to feel the effects of oversupply following peak ordering activity a decade ago.

It does remain to be seen how 2021’s vessel ordering activity, whether in the Cargo sectors or Offshore, will affect supply and demand balances across the different markets in the coming years.

VesselsValue data as of January 2021.

Disclaimer: The purpose of this blog is to provide general information and not to provide advice or guidance in relation to particular circumstances. Readers should not make decisions in reliance on any statement or opinion contained in this blog.

Want to know more about how our

data can help you assess the market?

Comments

Leave a Comment