Quarterly Forecast for Cargo Vessels: Summer 2020

Overview

Uncertainties surrounding the coronavirus outbreak, the trade war and volatility in oil prices are governing business decisions being made in 2020. Shipyard demand will likely encounter a further blow given the vast disruptions to economic growth and trade globally and delays to scrubber retrofits have already been seen and are expected to continue.

Containment measures and the potential for a resurgence of coronavirus remains a great uncertainty for global trade. Volatility in commodity prices has increased dramatically, complicating the outlook across the shipping markets.

To prop up economies central governments have released significant financial support to secure economic activity and thus seaborne demand post pandemic.

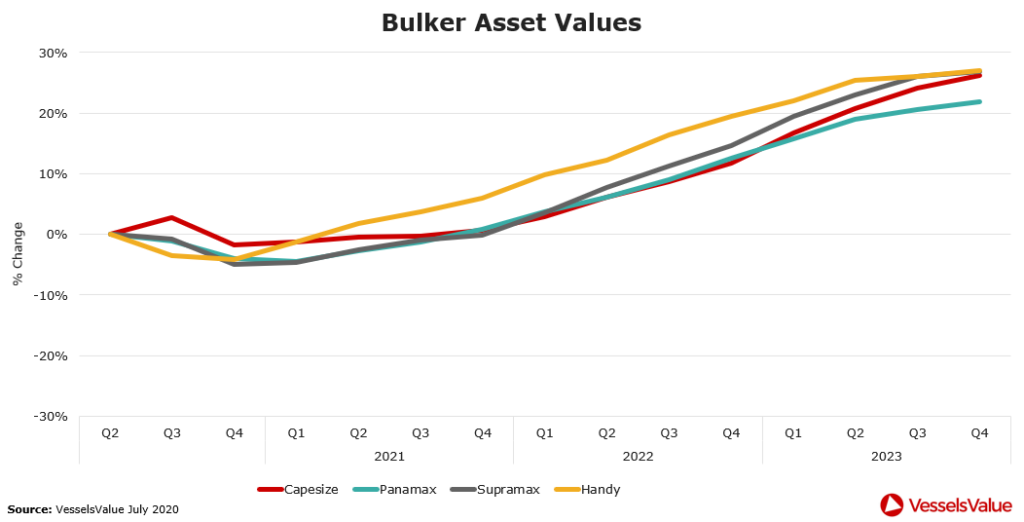

Bulker

- During the first half of 2020 the dramatic fall in freight rates and lower sale prices achieved on the secondhand S&P market led to a c.20% fall in older Bulker values.

- The low iron ore exports from Brazil have resulted in the depressed freight rates this spring. Capesize freight rates were hit hard, tumbling from 24,000 USD/day at the end of last year to about 2,200 USD/day at the beginning of March. This trickled down into the smaller sizes with Panamax, Supramax and Handy segments hitting lows in March/April. However, rates have improved significantly across all Bulkers since the beginning of June.

- Vale, the major Brazilian iron ore producer has reiterated its production guidance for the year, confident that volumes will return. The uptick of Brazilian export volumes into China resulted in the increased freight rates throughout June.

- With very few orders over the last couple of years and with only a handful having taken place in this year there is declining tonnage supply.

- Pent up demand for scrapping after all the beaches have been closed is expected to increase activity in the second half of 2020 and due to the reduced fleet capacity, supply growth is expected to rise going into 2021.

- From June onward, a tighter dry bulk market balance is expected due to the return of Brazilian iron ore volumes and Indian coal demand. The stimulus package in China and reopening of economic activity in many countries will give further support to a rebound of dry bulk freight rates and hence values.

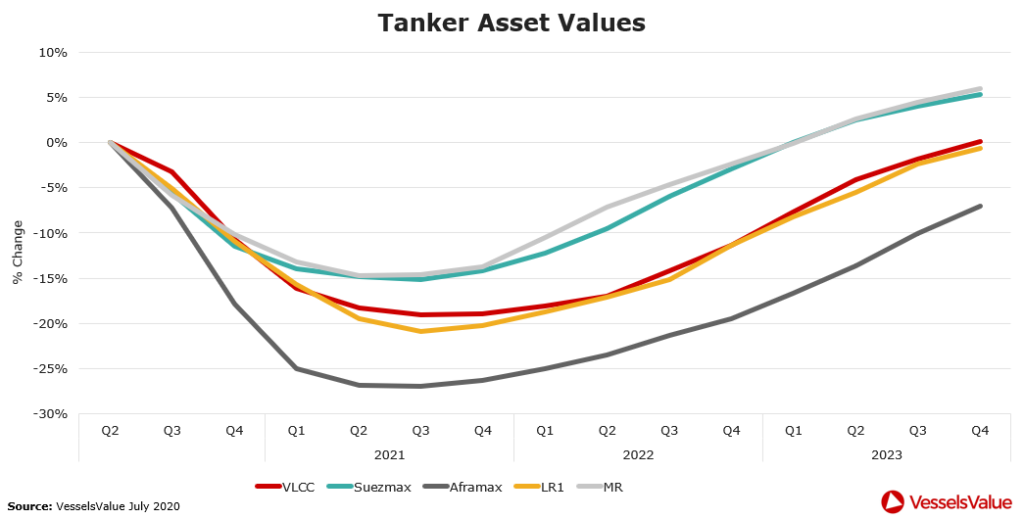

Tanker

- The beginning of Q2 2020 showed strong spot rates across the Tanker sector due to the surplus of cheap oil and demand for floating storage. However, the recent decline in spot rates have bought figures back down to normality.

- In April an OPEC+ agreement was reached which targets a cut in production of 9.7Mbd in May, June and July. With a decline in tonnage used for floating storage and the huge impact on demand from the coronavirus lockdowns, summer earnings are set for a massive correction.

- Again scrapping remained low due to the closure of all beaches. It is expected the second half of 2020 will show an increase in scrapping due to the pent up tonnage.

- New ordering activity is expected to remain low in the second half of 2020 due to the declining earnings.

- Following several quarters of appreciation in tanker values, values have started to stabilise. As earnings are set for a decline and ordering activity is expected to be low, we are expecting to see a slight softening to the values.

- The demand centers in China and Asia will post healthy import figures on crude volumes heading for storage and we are also expecting to see a rebound in industrial activity and consumer demand in the aftermath of the coronavirus.

- However, it is predicted the decline in US oil production will negatively impact US oil exports and remove a significant part of the long-haul trade to Asia that has developed over the past several years.

- That being said, forecast ton mile growth is strong for the rest of 2020.

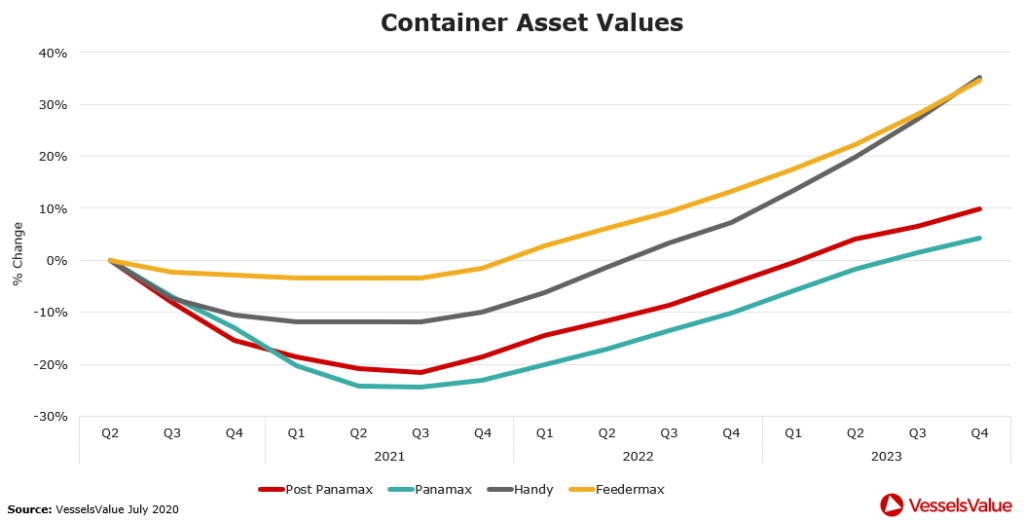

Container

- A massive drop in consumer demand as various countries locked down to contain the virus meant there has been an unprecedented collapse in box cargo volumes, comparable to the Financial Crisis, counted by a large amount of blanked sailings.

- This led to a drop in freight rates across all Container tonnage with the larger Post Panamax vessels down c.60% compared to mid February. Freight rates are predicted to continue to fall this year, although the steepest fall seems to be behind us.

- Newbuild orders have been low this year, a total of 5 ULCVs hit the water this spring, including the world’s largest container vessel, the 23,964 TEU HMM Algeciras in April.

- The vast majority of containerships undergoing delayed retrofits in China are part of the increasing idle numbers, which reached a staggering c.11.5% a week in May.

- It is expected global containerised trade (TEU-Miles) will decline by 10% in 2020 as a result of an economic contraction, manufacturers seeking to work through inventories and consumer demand dampened by high unemployment and social distancing. This collapse in TEU-Miles demand is one of the most substantial ever recorded.

- In most European countries retail sales are down almost 20% along with increased economic uncertainty, consumer confidence and household spending is expected to decline and Asia-Europe WB is expected to drop 13% in 2020.

- From 2021 a recovery in volumes is likely due to a rebound in manufacturing and private consumption, combined with easing trade tensions and clarity on the postponed Brexit trade agreement.

- Is it expected blanked sailings will decrease and reduce the idle numbers, hence increasing supply. The increased sailing distance in 2020 due to rerouting around the Cape of Good Hope instead of using the Suez Canal (to avoid canal fees when bunker prices are low) is also contributing to lowering supply. A potential rebound next year is dampened by vessels returning from retrofits and reduced practice of idling. A more substantial recovery is expected in 2022.

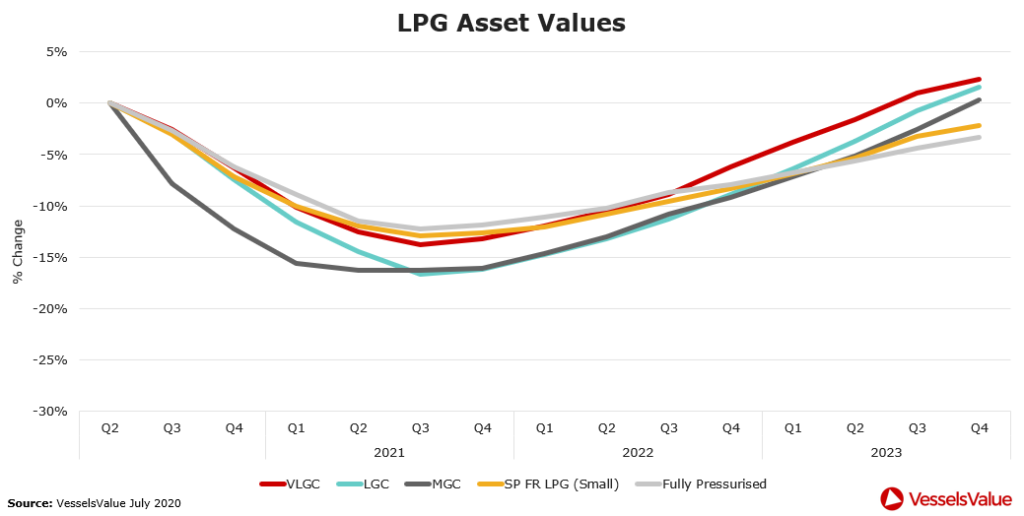

Gas

- In Q2 2020 we have seen the spot market earnings for VLGCs tumble from the highs of Q1 to levels just above OPEX. Lower US LPG export volumes driven by cutbacks in oil production in the wake of the Covid-19 pandemic are considered to be a main driver of this development. Middle East export of LPG is also trending lower on reduced oil production. In Europe, the low oil price has made naphtha a more attractive feedstock for crackers, reducing the sectors LPG demand.

- Petchem gases continue to ship to Asia, although total volumes are down from last year.

- Lower oil production in the US and Middle East will reduce the availability of the by-product LPG. Lower trade volumes will offset shipping demand and weaken the market balance as fleet growth in the short term will be firm.

- Lower earnings have bought values down for larger vessels however the lack of orders placed this year and a low fleet growth may provide some support for this sector going into 2021.