The Emergence of New Tanker Market Players

Since the start of the conflict between Ukraine and Russia, a new breed of Tanker owners has emerged. Demand for Tankers increased, and this has caused Tanker freight rates to rise following a long period of stagnation, enticing new players to enter the market.

Sanctions on Russian crude oil and clean petroleum products came into force in December 2022 and February 2023 respectively. As a result, this has curbed the trade in Russian crude oil to the West, followed by a shift in trade flow patterns.

This led to the emergence of new market players, who were keen to take advantage of the premiums available from carrying sanctioned cargoes, which traditional owners are no longer willing to carry. At the same time, this new entrants to the Tanker market have created a link that has enabled Russian oil to carry on flowing, with very little impact from the sanctions. Furthermore, cargoes have moved away from Europe to destinations further afield, such as China, India and the UAE.

Using VesselsValue data, we take a look at the new and opportunistic entrants who have appeared in the Tanker market. We analyse what they have bought, and the impact this had on respective market values, particularly as demand for older tonnage continues to boom.

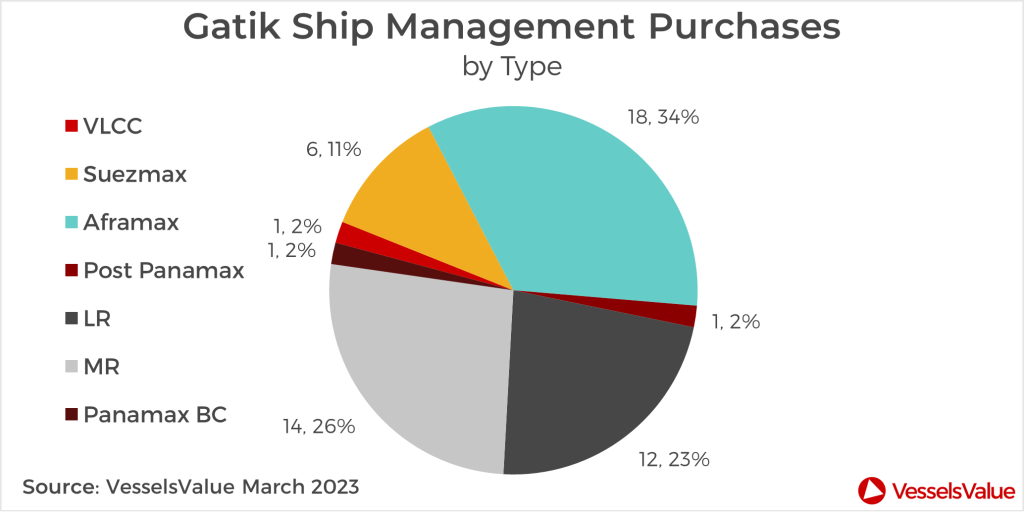

Gatik Ship Management

India based Gatik Ship Management is one of the most interesting companies to have emerged over the last 18 months. A previously unknown entity, the company has acquired and is now operating an astonishing 53 Tankers (37,100- 318,100 DWT) since December 2021, with an average age of 17 years and a total market value of USD 1.5 bn.

The majority of these purchases were in the Aframax / LR2 sector, accounting for almost half of purchases at c.49%. This sector has seen the largest jump in values out of all the Tanker sectors. Values for 20YO vessels of 105,000 DWT have increased by c.135% since the start of January 2022, from USD 11.84 mil to USD 27.84 mil.

MRs, including MR1s and MR2, were the second most popular vessels for Gatik, accounting for c.26%. Echoing the pattern seen in the Aframax sector, 20YO vessels of 45,000 DWT saw the second largest jump in values at c.120.24%, from a demolition value of USD 6.57 mil to USD 14.47 mil.

Suezmax Tankers ranked third, accounting for 11% of Gatik purchases so far. Here, values saw the third highest jump, moving up by c.95% from a demolition value of USD 15.92 mil to USD 31.02 mil.

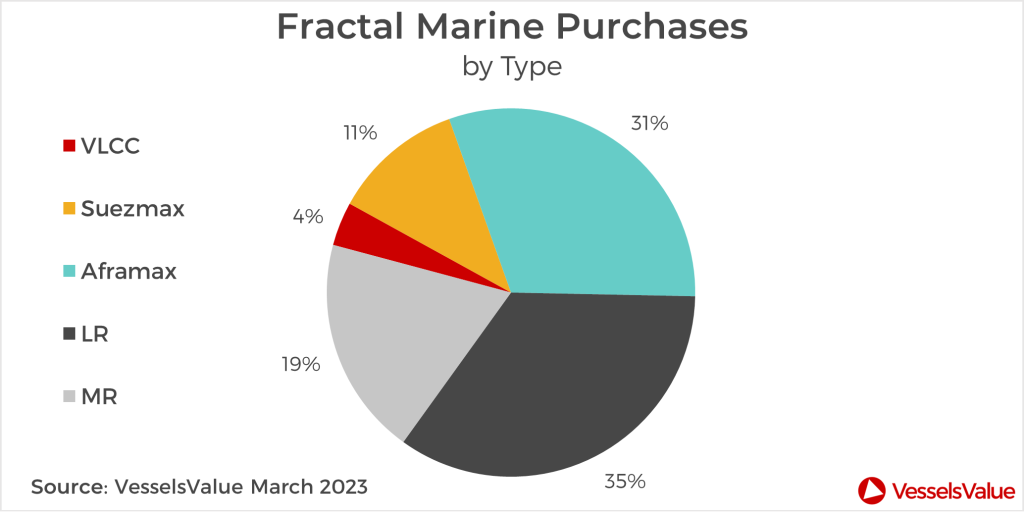

Fractal Marine Shipping

Fractal Marine Shipping is another new entrant to the market over the past year. Headquartered in Geneva and Registered in the UAE, Fractal are managing the commercial operation of Tankers. The company have put together a fleet of 27 vessels since March 2020, with 26 of these vessels having been bought since May 2022. The vessels bought are between 9 to 14 years of age, with an average age of the vessels purchased being 17 years.

Aframaxes / LR2s make up the majority of the Fractal fleet, accounting for c.42%, followed by LR1s with c.23% and MRs ranking third at c.19%.

Radiating World Shipping Services

UAE based Radiating World Shipping Services purchased their first vessel in December 2022 and since then they have acquired a total of 12 Tankers, including 6 Aframaxes and 6 MRs with an average age of 17 years.

Undisclosed buyers

So far this year alone, there have been 43 Tanker sales reported to undisclosed buyers, compared to just nine for the same period last year. These vessels have an average age of 18 years.

The favour of the month for some time has been the MR sector, which has accounted for c.33% of sales to undisclosed buyers this year, followed by Aframaxes/LR2s at c.25% and VLCCs ranking third at c.19%.

Conclusion

Overall, the combination of sales to Gatik, Fractal, Radiating World Shipping Services and undisclosed buyers this year accounts for a large proportion of sale and purchase transactions that have taken place. Around c.33% of Tanker sales. Outside of the above sales, the UAE ranked first with 23 sales, equating to c.12.1% and Turkey came second with 22 sales, amounting to c.11.6%. Greece and India ranked joint third place with 15 sales each, equating to c.7.9%.

These figures imply that purchases by this new breed of Tanker owner are driving demand for this sector, specifically for older tonnage of over 15 years. Thus, it indicates that a large proportion of sale and purchase activity is for vessels being sold with the intention of being traded on these newly formed routes which are controlling values at the moment.

Disclaimer: The purpose of this blog is to provide general information and not to provide advice or guidance in relation to particular circumstances. Readers should not make decisions in reliance on any statement or opinion contained in this blog.

Want to know more about how our

data can help you assess the market?